Hyperliquid: Institutional Demand, ETFs, and DAT Flows

By

José Sanchez, Kelvin Koh

Jun 17, 2026

Hyperliquid (HYPE) was the standout large-cap performer in May 2026, rising roughly 40% in a single week, putting it firmly among the top 10 crypto assets and overtaking Solana's fully diluted valuation for the first time. What is unusual is the composition of the move. Neither the September 2024 token launch nor the October 2025 HIP-3 mainnet upgrade was the catalyst. May's price appreciation was driven primarily by two institutional demand channels that arrived within weeks of each other: US-listed spot HYPE ETFs, and a single corporate treasury vehicle (PURR, Hyperliquid Strategies Inc) whose accumulation pace accelerated sharply, all layered on top of continued share gains against centralized exchanges.

PURR now holds approximately 22.3 million HYPE (2.33% of total supply, worth roughly $1.6 billion at current prices). The position was built in two phases. Around 12.5 million HYPE came in via the Rorschach Merger contribution that took the company public on December 2, 2025, paid in HSI equity rather than cash. The remaining ~9.7 million has been cash-purchased onchain, with a cumulative cash cost of approximately $345 million through May 28, implying a rolling weighted-average cost of roughly $35 per HYPE. That sits well below the $68 May-31 close, and gives PURR a meaningful cushion as the trade compounds.

The reflexive structure is the key feature, and at present it is working cleanly. PURR's equity trades at approximately 1.16x modified NAV: each share issued at $9.99 brings in $1.39 above its $8.60 NAV contribution, an accretive transaction for existing holders that gives management a rational incentive to accelerate issuance while the premium remains positive. The structure works in both directions. If the multiple compresses below 1.0x, equity issuance becomes value-destructive and the largest marginal buyer in May steps aside. Remaining cash on PURR's balance sheet stands at approximately $157 million, enough to extend the recent purchase pace for several additional weeks absent further capital raises.

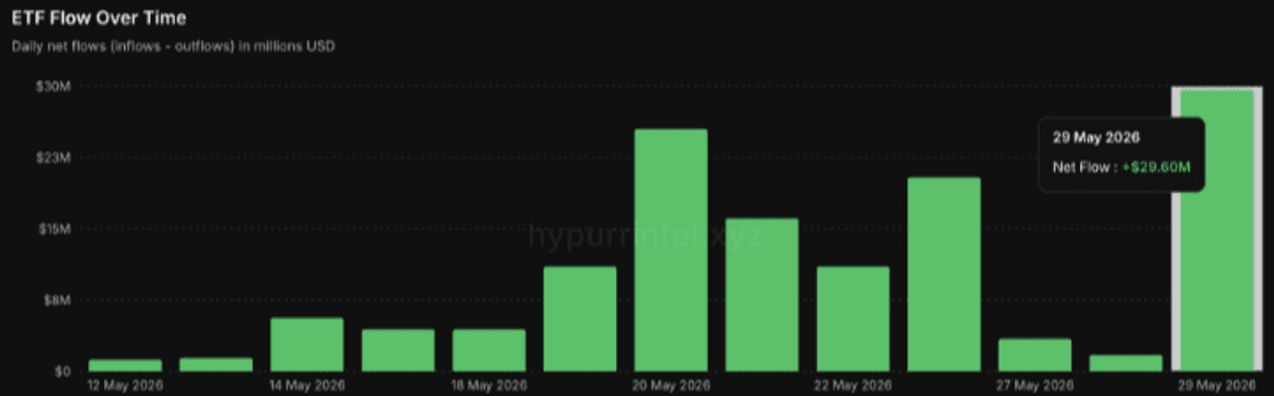

The second demand channel arrived in mid-May, when Bitwise and 21Shares launched spot HYPE ETFs: BHYP (0.34% fee) and THYP (0.30% fee). THYP began trading May 12, BHYP followed May 14. Combined inflows reached approximately $137.7 million across the first thirteen trading days through May 29 ($81.7M BHYP, $56.0M THYP), with holdings now around 2.3 million HYPE (0.24% of supply). Flow has not tapered the way new crypto ETF launches typically do: $25.5 million arrived on May 20, $20.4 million on May 26, and a new single-day high of $31.6 million printed on May 29.

HYPE has benefitted from steady ETF inflows

Source: PURR

The relevant precedent is Bitwise's BSOL launch on October 28, 2025: $358 million in inflows across the first 14 days with no outflow sessions, followed by SOL declining 35% over the next three months as the demand pulse front-loaded and trailing daily inflows tapered to roughly $12 million. HYPE ETF inflows have run at roughly 38% of BSOL's launch-window pace, slower in absolute terms but without yet showing the front-loaded taper BSOL exhibited.

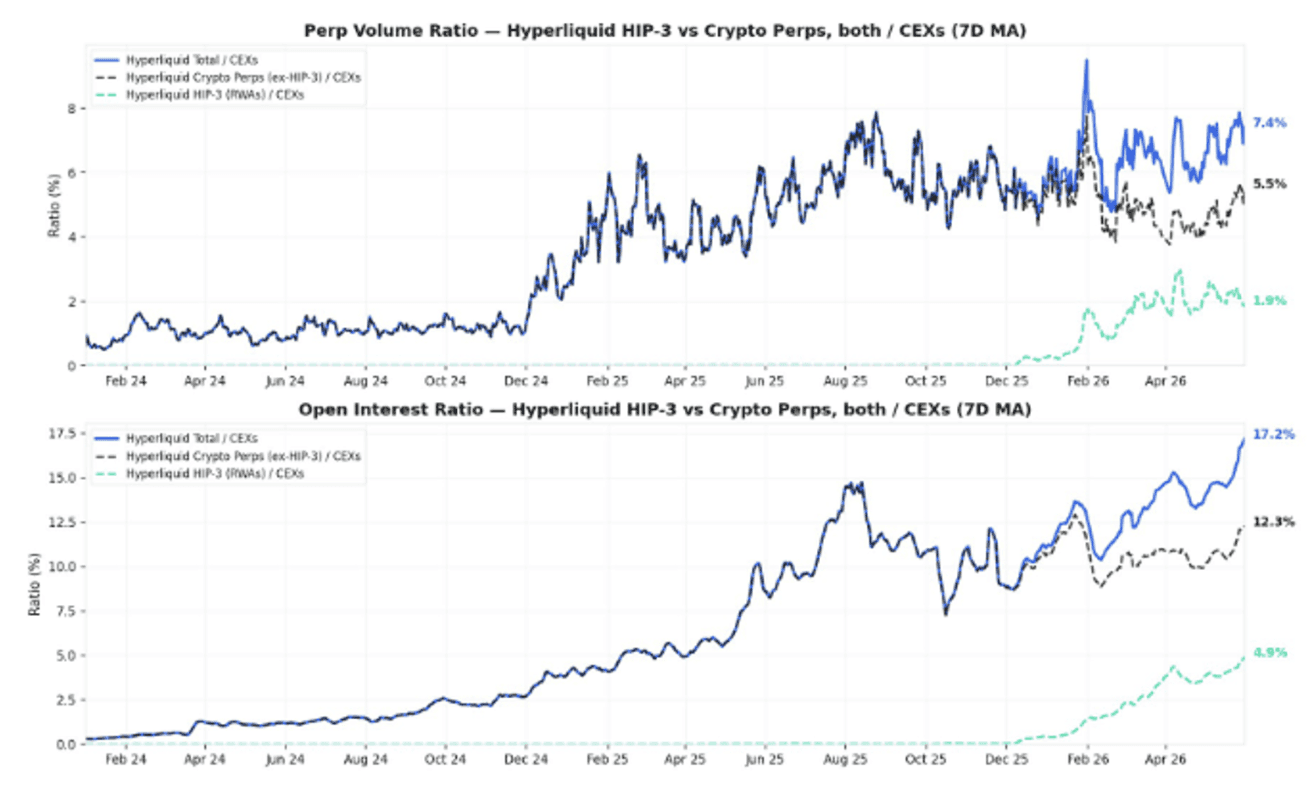

Underpinning the flow story, Hyperliquid has continued to gain share against centralized exchanges in both volume and open interest, at a rate that distinguishes it from any other onchain venue. On a 7-day moving average through May 31, Hyperliquid captures approximately 7.4% of total CEX perpetual volume (5.5% crypto plus 1.9% HIP-3) and 17.2% of CEX open interest (12.3% crypto plus 4.9% HIP-3).

The HIP-3 figure is notable: the standard only went live on mainnet in October 2025, meaning roughly 5 percentage points of CEX-relative OI share have been built in seven months from equity, commodity, and FX perpetuals that did not exist onchain before.

Hyperliquid continues to gain market share against centralized exchanges

Source: Spartan Capital

Competitive validation arrived in May. Binance has progressively launched its own perpetual contracts for the same equity, commodity, and FX tickers that Hyperliquid pioneered onchain via HIP-3 deployers such as Trade.XYZ, including single-stock perps for major US tech names and a slate of metals and FX pairs. This is the standard centralized-exchange response to a new category proving demand, and the first credible competitive threat to HIP-3 deployers' first-mover advantage.

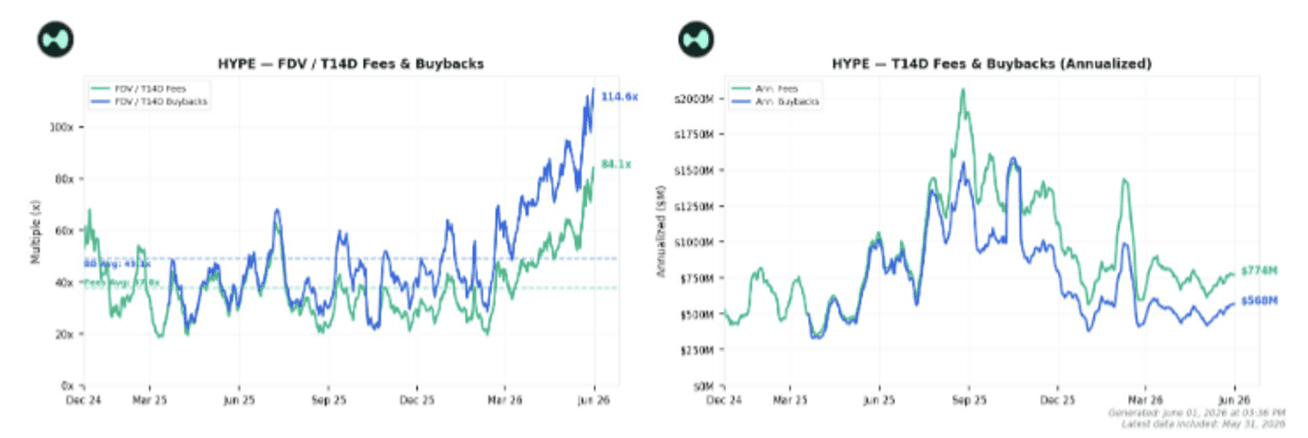

Against this backdrop, Hyperliquid’s absolute fee picture softened through the first half of 2026 but stabilized in recent weeks. Annualized crypto perpetual fees fell from $832 million in January to $642 million in May, a 23% contraction as venue volumes compressed from cycle peaks. HIP-3 added $39 million annualized in May (vs. $31 million in January), which does not offset the crypto perps fee decline. Total combined platform fees ran at $905 million annualized in January and $721 million on a May monthly basis but firmed back to approximately $774 million on a trailing 14-day window through May 31, with the buyback program running at $568 million annualized. Against $68.8 billion FDV, FDV-to-fees stands at 84x and FDV-to-buybacks at 115x, both at all-time highs as the price rally has outpaced the recent fee firming.

Hyperliquid’s valuation multiple has risen significantly since March 2026

Source: Spartan Capital

The recently announced AQAv2 mechanism would route a share of yield from Hypercore's $5.21 billion USDC reserves back to the protocol treasury. At a 3.5% T-bill yield and the proposed 40% to 90% take-rate range, this would add $73 to $164 million in annualized revenue, a 9% to 21% uplift to the trailing fee base. At the high end, combined fees would reach approximately $938 million, implying an FDV-to-fees multiple of approximately 73x.

A few observations that are worth tracking from here. The demand stack is more concentrated than the headline framing suggests: PURR and two newly launched ETFs accounted for most marginal flow in May, and any single channel pausing could compress the trade quickly. The PURR reflexive loop depends on the mNAV premium staying positive; if HYPE underperforms or PURR's equity de-rates toward parity, accretive issuance stops. The Binance HIP-3-equivalent listings are the first direct competitive response to the non-crypto perpetual category, and the share-gain trajectory there will need to be re-evaluated against a venue with deeper distribution and balance-sheet capacity. There is also the fact that CME has filed a complaint with the CFTC regarding Hyperliquid's offering of unregistered derivatives to US persons, introducing a binary regulatory risk.

All in all, Hyperliquid has transitioned from a single perpetual-fee story into a multi-driver platform story. The crypto perpetuals business that generated the original 2024-2025 thesis is now one of several drivers, alongside a HIP-3 RWA category that has built nearly five percentage points of CEX-relative OI share in seven months, a buyback engine recycling over half a billion dollars annually into supply reduction, and institutional buying channels through corporate treasury vehicles and US-listed ETFs. Whether the May re-rating reflects a new equilibrium or a flow-driven dislocation is the open question. The historical pattern for token-treasury vehicles and early ETF inflows suggests the first four to six weeks are not predictive of steady-state flows, while the fundamental fee trajectory has stabilized but not turned upward. For Hyperliquid to grow into its $68.8 billion FDV at a 30x fee multiple, fees would need to roughly 3x from current trailing levels. The next 60 days of ETF, PURR, share, and fee data will determine whether May marks a structural repricing or a flow-driven peak.

Hyperliquid (HYPE) was the standout large-cap performer in May 2026, rising roughly 40% in a single week, putting it firmly among the top 10 crypto assets and overtaking Solana's fully diluted valuation for the first time. What is unusual is the composition of the move. Neither the September 2024 token launch nor the October 2025 HIP-3 mainnet upgrade was the catalyst. May's price appreciation was driven primarily by two institutional demand channels that arrived within weeks of each other: US-listed spot HYPE ETFs, and a single corporate treasury vehicle (PURR, Hyperliquid Strategies Inc) whose accumulation pace accelerated sharply, all layered on top of continued share gains against centralized exchanges.

PURR now holds approximately 22.3 million HYPE (2.33% of total supply, worth roughly $1.6 billion at current prices). The position was built in two phases. Around 12.5 million HYPE came in via the Rorschach Merger contribution that took the company public on December 2, 2025, paid in HSI equity rather than cash. The remaining ~9.7 million has been cash-purchased onchain, with a cumulative cash cost of approximately $345 million through May 28, implying a rolling weighted-average cost of roughly $35 per HYPE. That sits well below the $68 May-31 close, and gives PURR a meaningful cushion as the trade compounds.

The reflexive structure is the key feature, and at present it is working cleanly. PURR's equity trades at approximately 1.16x modified NAV: each share issued at $9.99 brings in $1.39 above its $8.60 NAV contribution, an accretive transaction for existing holders that gives management a rational incentive to accelerate issuance while the premium remains positive. The structure works in both directions. If the multiple compresses below 1.0x, equity issuance becomes value-destructive and the largest marginal buyer in May steps aside. Remaining cash on PURR's balance sheet stands at approximately $157 million, enough to extend the recent purchase pace for several additional weeks absent further capital raises.

The second demand channel arrived in mid-May, when Bitwise and 21Shares launched spot HYPE ETFs: BHYP (0.34% fee) and THYP (0.30% fee). THYP began trading May 12, BHYP followed May 14. Combined inflows reached approximately $137.7 million across the first thirteen trading days through May 29 ($81.7M BHYP, $56.0M THYP), with holdings now around 2.3 million HYPE (0.24% of supply). Flow has not tapered the way new crypto ETF launches typically do: $25.5 million arrived on May 20, $20.4 million on May 26, and a new single-day high of $31.6 million printed on May 29.

HYPE has benefitted from steady ETF inflows

Source: PURR

The relevant precedent is Bitwise's BSOL launch on October 28, 2025: $358 million in inflows across the first 14 days with no outflow sessions, followed by SOL declining 35% over the next three months as the demand pulse front-loaded and trailing daily inflows tapered to roughly $12 million. HYPE ETF inflows have run at roughly 38% of BSOL's launch-window pace, slower in absolute terms but without yet showing the front-loaded taper BSOL exhibited.

Underpinning the flow story, Hyperliquid has continued to gain share against centralized exchanges in both volume and open interest, at a rate that distinguishes it from any other onchain venue. On a 7-day moving average through May 31, Hyperliquid captures approximately 7.4% of total CEX perpetual volume (5.5% crypto plus 1.9% HIP-3) and 17.2% of CEX open interest (12.3% crypto plus 4.9% HIP-3).

The HIP-3 figure is notable: the standard only went live on mainnet in October 2025, meaning roughly 5 percentage points of CEX-relative OI share have been built in seven months from equity, commodity, and FX perpetuals that did not exist onchain before.

Hyperliquid continues to gain market share against centralized exchanges

Source: Spartan Capital

Competitive validation arrived in May. Binance has progressively launched its own perpetual contracts for the same equity, commodity, and FX tickers that Hyperliquid pioneered onchain via HIP-3 deployers such as Trade.XYZ, including single-stock perps for major US tech names and a slate of metals and FX pairs. This is the standard centralized-exchange response to a new category proving demand, and the first credible competitive threat to HIP-3 deployers' first-mover advantage.

Against this backdrop, Hyperliquid’s absolute fee picture softened through the first half of 2026 but stabilized in recent weeks. Annualized crypto perpetual fees fell from $832 million in January to $642 million in May, a 23% contraction as venue volumes compressed from cycle peaks. HIP-3 added $39 million annualized in May (vs. $31 million in January), which does not offset the crypto perps fee decline. Total combined platform fees ran at $905 million annualized in January and $721 million on a May monthly basis but firmed back to approximately $774 million on a trailing 14-day window through May 31, with the buyback program running at $568 million annualized. Against $68.8 billion FDV, FDV-to-fees stands at 84x and FDV-to-buybacks at 115x, both at all-time highs as the price rally has outpaced the recent fee firming.

Hyperliquid’s valuation multiple has risen significantly since March 2026

Source: Spartan Capital

The recently announced AQAv2 mechanism would route a share of yield from Hypercore's $5.21 billion USDC reserves back to the protocol treasury. At a 3.5% T-bill yield and the proposed 40% to 90% take-rate range, this would add $73 to $164 million in annualized revenue, a 9% to 21% uplift to the trailing fee base. At the high end, combined fees would reach approximately $938 million, implying an FDV-to-fees multiple of approximately 73x.

A few observations that are worth tracking from here. The demand stack is more concentrated than the headline framing suggests: PURR and two newly launched ETFs accounted for most marginal flow in May, and any single channel pausing could compress the trade quickly. The PURR reflexive loop depends on the mNAV premium staying positive; if HYPE underperforms or PURR's equity de-rates toward parity, accretive issuance stops. The Binance HIP-3-equivalent listings are the first direct competitive response to the non-crypto perpetual category, and the share-gain trajectory there will need to be re-evaluated against a venue with deeper distribution and balance-sheet capacity. There is also the fact that CME has filed a complaint with the CFTC regarding Hyperliquid's offering of unregistered derivatives to US persons, introducing a binary regulatory risk.

All in all, Hyperliquid has transitioned from a single perpetual-fee story into a multi-driver platform story. The crypto perpetuals business that generated the original 2024-2025 thesis is now one of several drivers, alongside a HIP-3 RWA category that has built nearly five percentage points of CEX-relative OI share in seven months, a buyback engine recycling over half a billion dollars annually into supply reduction, and institutional buying channels through corporate treasury vehicles and US-listed ETFs. Whether the May re-rating reflects a new equilibrium or a flow-driven dislocation is the open question. The historical pattern for token-treasury vehicles and early ETF inflows suggests the first four to six weeks are not predictive of steady-state flows, while the fundamental fee trajectory has stabilized but not turned upward. For Hyperliquid to grow into its $68.8 billion FDV at a 30x fee multiple, fees would need to roughly 3x from current trailing levels. The next 60 days of ETF, PURR, share, and fee data will determine whether May marks a structural repricing or a flow-driven peak.

To learn more about investment opportunities with Spartan Capital, please contact ir@spartangroup.io