Strategy: From Flywheel to Framework

By

Patrick Forster, Kelvin Koh

Jul 17, 2026

On June 27, 2026, Strategy’s mNAV — enterprise value measured against its Bitcoin holdings — closed below 1.0x for the first time in its six-year history. Two days later, Strategy announced its new ‘Digital Credit Capital Framework’, a five-part overhaul of its capital structure, designed to bring confidence back to investors who were beginning to see the writing on the wall and making it known through its stock price. Within a week, Strategy announced it had sold 3,588 BTC (~$216 million) to fund preferred dividends — the largest sale in its history and an abandoning of the ‘never sell’ mantra. So how did we get here? And what does the path forward look like?

Strategy’s mNAV has been declining steadily in the past few months

Source: StrategyTracker.com, company filings and Spartan Capital estimates.

When we last covered DATs in our August 2025 newsletter, MSTR traded at 1.7x the value of its then - 628,946 BTC, and the premium-issuance flywheel made every raise accretive for shareholders as BTC per share rose. Below 1.0x, however, the flywheel inverts — issuance dilutes — while the liability side stands still: roughly $441 million a quarter (~$1.76 billion a year) of preferred dividends and interest across STRC, STRF, STRD, STRK, STRE and its convertible instruments, against an asset that yields nothing. When the premium disappears, the ‘free money’ funding mechanism goes along with it and is replaced by the question: where are we going to get $1.76 billion a year?

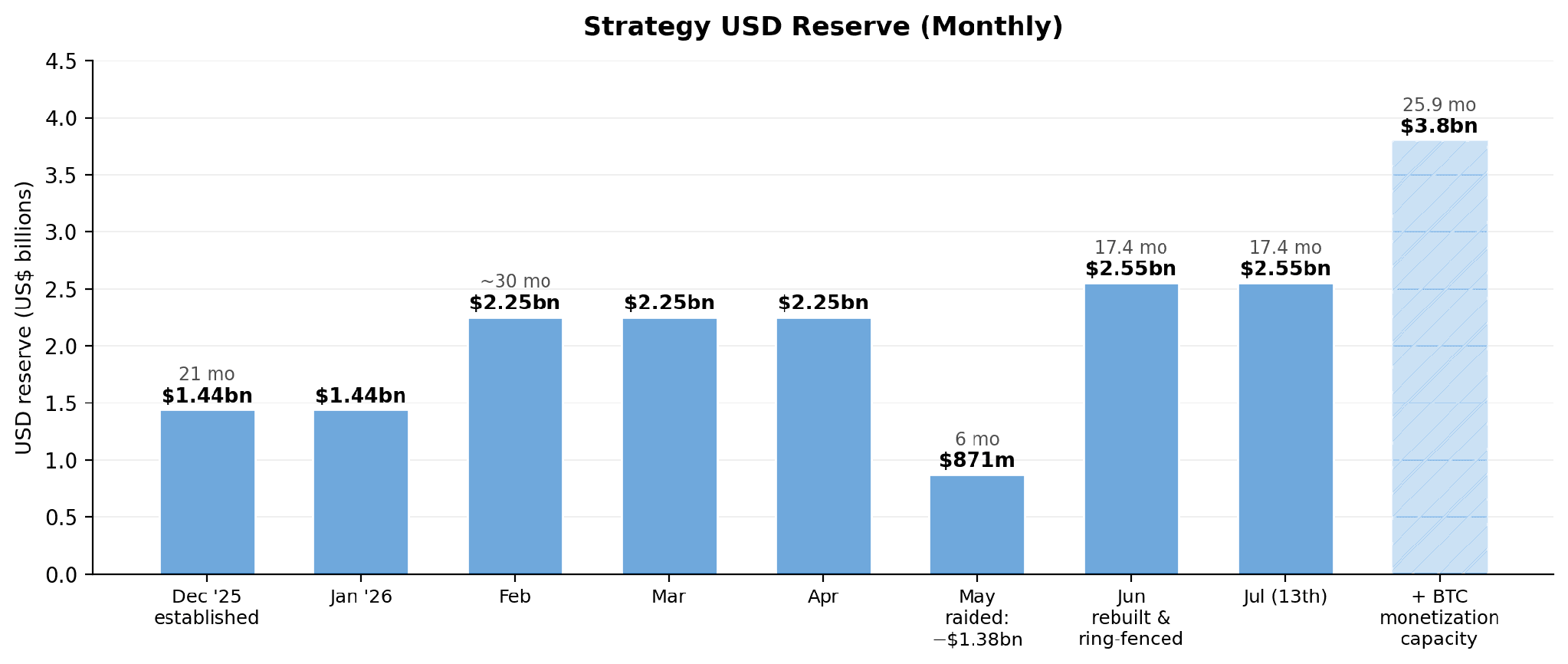

Although there has been a litany of questionable decisions from the company, none catalyzed the decline more than this: the decision to repurchase $1.5 billion of its 0% 2029 converts for ~$1.38 billion on May 15, 2026. On face value, this doesn’t seem too bad; an 8% discount to par, marketed to equity holders as a “BTC Gain” of 4,391 BTC. Eleven days later, however, they announced the funding source — the USD cash reserve that had been established six months earlier to backstop dividend payments, particularly for STRC. Initially seeded with $1.44 billion, the USD reserve was structured to fund at least 12 months of dividend and interest obligations, with a stated intention to strengthen over time and ultimately cover 24 months or more. At the same time, Strategy issued another $2 billion of 11.5% STRC to buy Bitcoin, adding approximately $230 million of annual dividends. Overnight, the USD reserve had collapsed from $2.25 billion to $871 million, and the dividend coverage fell from 16 months to 6 months.

Strategy compounded this mistake on June 1, 2026, when they elected to sell 32 BTC. It was meant to reassure preferred holders that they could monetize BTC to fund dividends. Instead, it spooked MSTR and BTC holders who also saw the same thing. By the end of June, Bitcoin traded below $60,000, STRC fell into the mid-$70s and MSTR’s mNAV dropped below 1.0x.

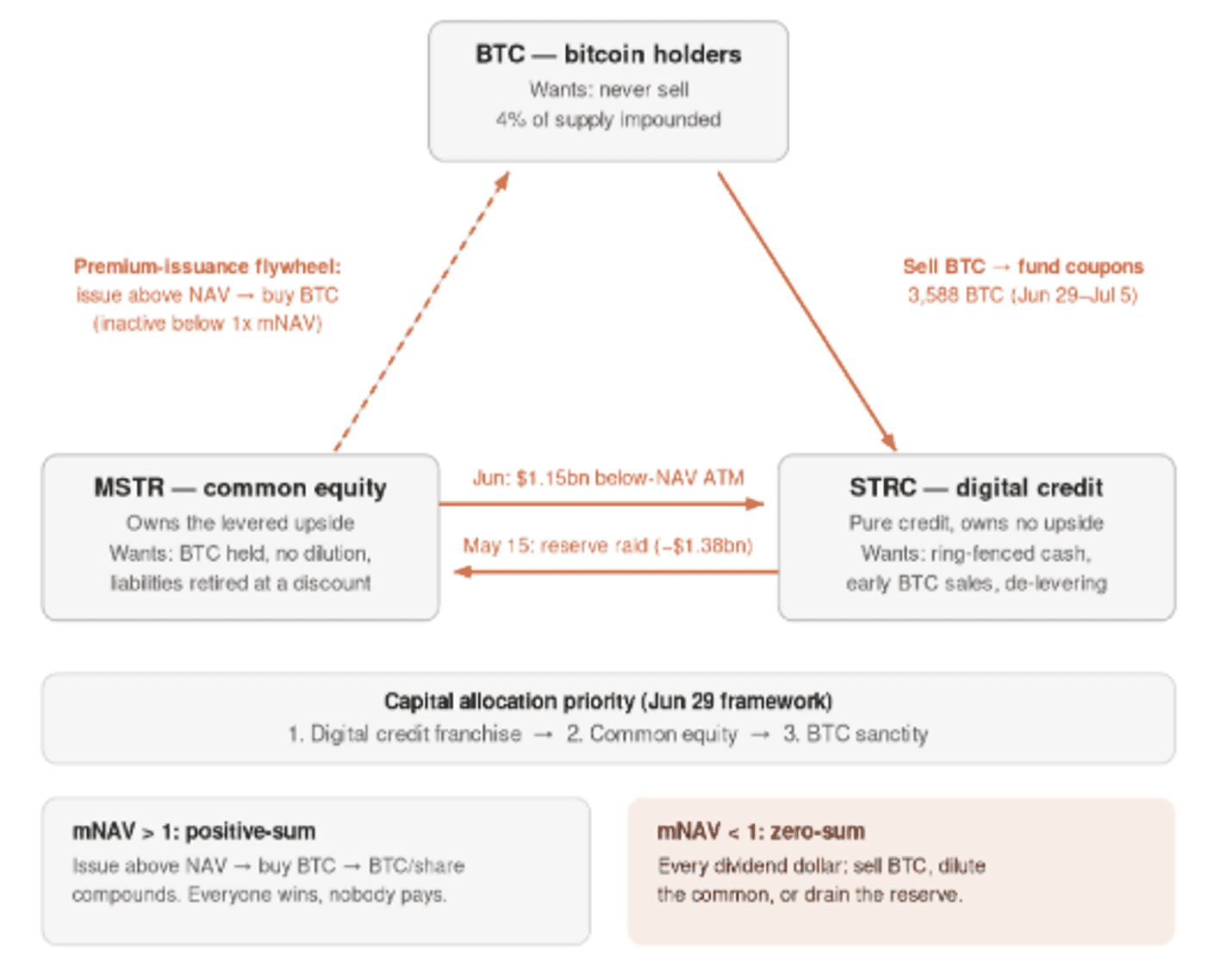

This exposed the central problem confronting Strategy. Without the premium, funding decisions are no longer positive sum, they are zero-sum at best. To give to one you must take from the other. And each cohort has conflicting incentives. MSTR holders own the levered residual upside, so they want Strategy to maximize bitcoin per share by retaining BTC, avoiding below-NAV dilution and retiring liabilities at discounts. STRC holders own an income claim with little participation in Bitcoin’s upside, so they prioritize funded liquidity, payment certainty and a willingness to monetize BTC when necessary. Bitcoin holders own the underlying scarce asset and have treated Strategy as a permanent source of demand, so they want the company to remain a net accumulator and fund its obligations without returning BTC to the market. Although Strategy’s new Digital Credit Capital Framework does not eliminate this incentive triangle, it does formalize how management will respond and allocate capital among the competing claims.

Strategy’s Incentive Triangle

Source: Spartan Capital

Strategy’s Digital Credit Capital Framework

USD Reserve Policy: Ring-fences the reserve — rebuilt to $2.55 billion, roughly 17.4 months of coverage — exclusively for dividend and interest payments, with a Board-mandated 12-month minimum. It directly addresses May’s lesson: the reserve can no longer be repurposed without explicit Board authorization.

Revised STRC Dividend Policy: Adjusts STRC’s yield monthly to keep it near $100 — the rate was raised from 11.5% to 12.0% effective July 1, with an explicit corporate objective for STRC to trade between $99 and $100.

Digital Credit Repurchase Program: Allows Strategy to buy back up to $1 billion of discounted preferreds, giving holders a potential price backstop while reducing the company’s future dividend burden.

MSTR Repurchase Program: Lets Strategy support the common stock with up to $1 billion of repurchases when it trades below intrinsic value, reassuring shareholders that management will not only issue and dilute equity.

BTC Monetization Program: Permits BTC sales for three bounded purposes: up to $1.25 billion to fund the USD Reserve, funding the two $1 billion repurchase programs, and covering dividends and interest as they fall due; anything beyond requires fresh Board authorization. Combined with the reserve, the $1.25 billion capacity lifts dividend liquidity coverage to approximately $3.8 billion (~26 months).

In our view, the USD reserve policy and the Digital Credit Repurchase Program are the most important introductions. Ringfencing the USD reserve and implementing a 12-month minimum runway was crucial because it separated Strategy’s near-term cash obligations from BTC and eliminated the potential for it to be repurposed, as seen previously when the 0% 2029 converts were repurchased in May.

Strategy has restored its USD reserve to above pre-May 2026 levels

Source: Company filings and Spartan Capital estimates.

Establishing the Digital Credit Repurchase Program lifted Strategy into a less vulnerable position by giving them a tool to stop self-reinforcing weakness from turning into a crisis. If STRC trades significantly below par, they can repurchase it at a discount, thereby reducing cash obligations and passing the discount through to MSTR holders. Retiring STRC at $75 removes a full $100 of liability and a 12% perpetual coupon — roughly a 16% yield on cost. Regardless of whether they need to do this in the future or not, the capability alone should reduce speculative pressure on STRC by introducing a credible potential buyer.

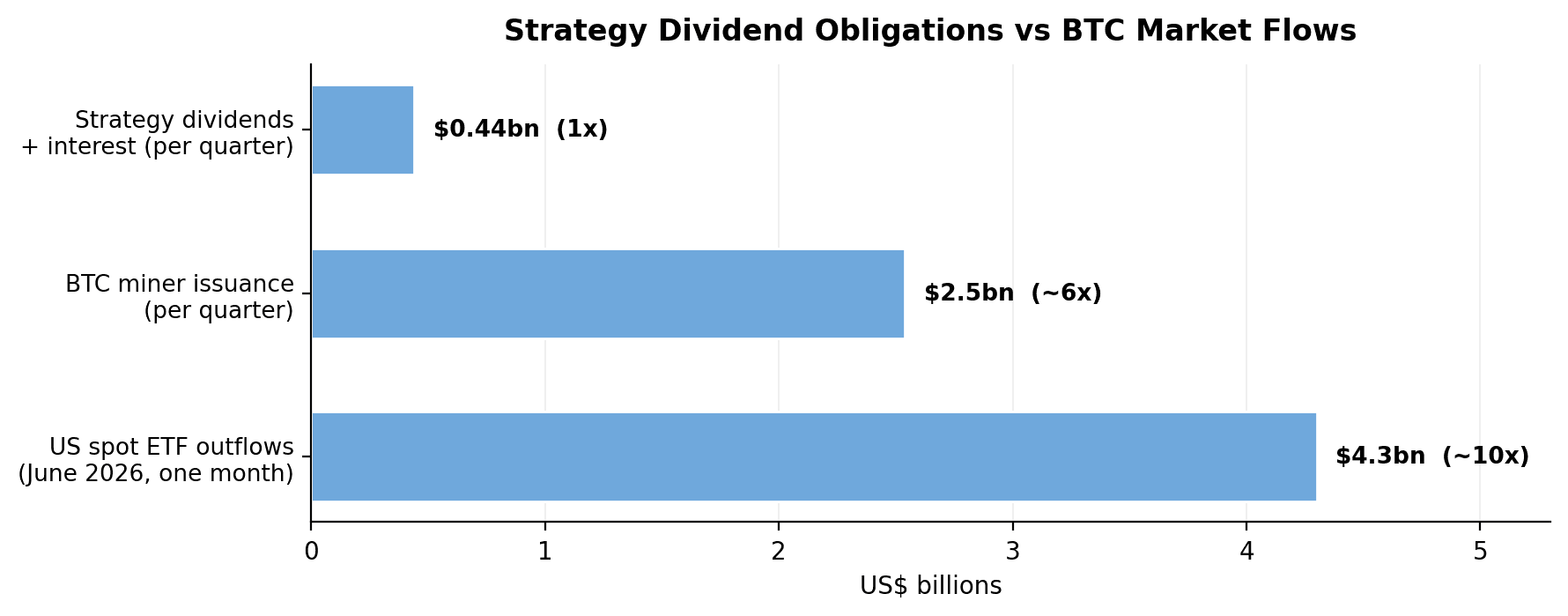

Going forward, Strategy has approximately $441 million in dividend obligations per quarter, with ¾ of this coming from STRC. Assuming these are funded exclusively from BTC sales, it would translate into $4.9 million in sales per day. The market can easily absorb this amount with no discernible price impact, given aggregate daily BTC spot volume of around $9.67 billion. For comparison, sell-pressure from BTC miners @ 450 BTC per day is around $28 million, meaning that sell pressure from Strategy is < 20% of that from miners.

In fact, the net BTC ETF flows for June were -$4.3 billion - 10x Strategy’s quarterly obligations. In other words, June’s ETF outflows averaged the equivalent of one full month of Strategy’s obligations every day, for 30 consecutive days. The key insight from this is that the actual expected sell pressure from Strategy to fund their dividend obligations is less significant than the paradigm shift from them being a pure accumulator to running an active strategy. The open question is how much of this has already been priced in, given the aggressive moves we’ve seen following Strategy’s first 32 BTC sale.

Strategy’s quarterly dividend obligations are a fraction of BTC market flows

Source: Company filings, Farside Investors, Spartan estimates.

The first indication came on July 6, when an 8-K disclosed that Strategy had sold 3,588 BTC ($216 million). Bitcoin dipped on the headline, then reversed within hours to above where it traded before the framework was announced. With roughly 26 months of dividend coverage, accretive buybacks available across the capital structure for the first time, and 843,775 BTC of collateral, fears of Strategy becoming a capitulatory forced seller are overblown. The more likely and boring answer is that they must gradually unwind their capital stack through a mixture of opportunistic BTC sales and MSTR / STRC re-purchases. While that process stabilizes the balance sheet, it also weakens the reflexive upside potential of MSTR, dampening the attraction which drew so many investors to it in the first place.

On June 27, 2026, Strategy’s mNAV — enterprise value measured against its Bitcoin holdings — closed below 1.0x for the first time in its six-year history. Two days later, Strategy announced its new ‘Digital Credit Capital Framework’, a five-part overhaul of its capital structure, designed to bring confidence back to investors who were beginning to see the writing on the wall and making it known through its stock price. Within a week, Strategy announced it had sold 3,588 BTC (~$216 million) to fund preferred dividends — the largest sale in its history and an abandoning of the ‘never sell’ mantra. So how did we get here? And what does the path forward look like?

Strategy’s mNAV has been declining steadily in the past few months

Source: StrategyTracker.com, company filings and Spartan Capital estimates.

When we last covered DATs in our August 2025 newsletter, MSTR traded at 1.7x the value of its then - 628,946 BTC, and the premium-issuance flywheel made every raise accretive for shareholders as BTC per share rose. Below 1.0x, however, the flywheel inverts — issuance dilutes — while the liability side stands still: roughly $441 million a quarter (~$1.76 billion a year) of preferred dividends and interest across STRC, STRF, STRD, STRK, STRE and its convertible instruments, against an asset that yields nothing. When the premium disappears, the ‘free money’ funding mechanism goes along with it and is replaced by the question: where are we going to get $1.76 billion a year?

Although there has been a litany of questionable decisions from the company, none catalyzed the decline more than this: the decision to repurchase $1.5 billion of its 0% 2029 converts for ~$1.38 billion on May 15, 2026. On face value, this doesn’t seem too bad; an 8% discount to par, marketed to equity holders as a “BTC Gain” of 4,391 BTC. Eleven days later, however, they announced the funding source — the USD cash reserve that had been established six months earlier to backstop dividend payments, particularly for STRC. Initially seeded with $1.44 billion, the USD reserve was structured to fund at least 12 months of dividend and interest obligations, with a stated intention to strengthen over time and ultimately cover 24 months or more. At the same time, Strategy issued another $2 billion of 11.5% STRC to buy Bitcoin, adding approximately $230 million of annual dividends. Overnight, the USD reserve had collapsed from $2.25 billion to $871 million, and the dividend coverage fell from 16 months to 6 months.

Strategy compounded this mistake on June 1, 2026, when they elected to sell 32 BTC. It was meant to reassure preferred holders that they could monetize BTC to fund dividends. Instead, it spooked MSTR and BTC holders who also saw the same thing. By the end of June, Bitcoin traded below $60,000, STRC fell into the mid-$70s and MSTR’s mNAV dropped below 1.0x.

This exposed the central problem confronting Strategy. Without the premium, funding decisions are no longer positive sum, they are zero-sum at best. To give to one you must take from the other. And each cohort has conflicting incentives. MSTR holders own the levered residual upside, so they want Strategy to maximize bitcoin per share by retaining BTC, avoiding below-NAV dilution and retiring liabilities at discounts. STRC holders own an income claim with little participation in Bitcoin’s upside, so they prioritize funded liquidity, payment certainty and a willingness to monetize BTC when necessary. Bitcoin holders own the underlying scarce asset and have treated Strategy as a permanent source of demand, so they want the company to remain a net accumulator and fund its obligations without returning BTC to the market. Although Strategy’s new Digital Credit Capital Framework does not eliminate this incentive triangle, it does formalize how management will respond and allocate capital among the competing claims.

Strategy’s Incentive Triangle

Source: Spartan Capital

Strategy’s Digital Credit Capital Framework

USD Reserve Policy: Ring-fences the reserve — rebuilt to $2.55 billion, roughly 17.4 months of coverage — exclusively for dividend and interest payments, with a Board-mandated 12-month minimum. It directly addresses May’s lesson: the reserve can no longer be repurposed without explicit Board authorization.

Revised STRC Dividend Policy: Adjusts STRC’s yield monthly to keep it near $100 — the rate was raised from 11.5% to 12.0% effective July 1, with an explicit corporate objective for STRC to trade between $99 and $100.

Digital Credit Repurchase Program: Allows Strategy to buy back up to $1 billion of discounted preferreds, giving holders a potential price backstop while reducing the company’s future dividend burden.

MSTR Repurchase Program: Lets Strategy support the common stock with up to $1 billion of repurchases when it trades below intrinsic value, reassuring shareholders that management will not only issue and dilute equity.

BTC Monetization Program: Permits BTC sales for three bounded purposes: up to $1.25 billion to fund the USD Reserve, funding the two $1 billion repurchase programs, and covering dividends and interest as they fall due; anything beyond requires fresh Board authorization. Combined with the reserve, the $1.25 billion capacity lifts dividend liquidity coverage to approximately $3.8 billion (~26 months).

In our view, the USD reserve policy and the Digital Credit Repurchase Program are the most important introductions. Ringfencing the USD reserve and implementing a 12-month minimum runway was crucial because it separated Strategy’s near-term cash obligations from BTC and eliminated the potential for it to be repurposed, as seen previously when the 0% 2029 converts were repurchased in May.

Strategy has restored its USD reserve to above pre-May 2026 levels

Source: Company filings and Spartan Capital estimates.

Establishing the Digital Credit Repurchase Program lifted Strategy into a less vulnerable position by giving them a tool to stop self-reinforcing weakness from turning into a crisis. If STRC trades significantly below par, they can repurchase it at a discount, thereby reducing cash obligations and passing the discount through to MSTR holders. Retiring STRC at $75 removes a full $100 of liability and a 12% perpetual coupon — roughly a 16% yield on cost. Regardless of whether they need to do this in the future or not, the capability alone should reduce speculative pressure on STRC by introducing a credible potential buyer.

Going forward, Strategy has approximately $441 million in dividend obligations per quarter, with ¾ of this coming from STRC. Assuming these are funded exclusively from BTC sales, it would translate into $4.9 million in sales per day. The market can easily absorb this amount with no discernible price impact, given aggregate daily BTC spot volume of around $9.67 billion. For comparison, sell-pressure from BTC miners @ 450 BTC per day is around $28 million, meaning that sell pressure from Strategy is < 20% of that from miners.

In fact, the net BTC ETF flows for June were -$4.3 billion - 10x Strategy’s quarterly obligations. In other words, June’s ETF outflows averaged the equivalent of one full month of Strategy’s obligations every day, for 30 consecutive days. The key insight from this is that the actual expected sell pressure from Strategy to fund their dividend obligations is less significant than the paradigm shift from them being a pure accumulator to running an active strategy. The open question is how much of this has already been priced in, given the aggressive moves we’ve seen following Strategy’s first 32 BTC sale.

Strategy’s quarterly dividend obligations are a fraction of BTC market flows

Source: Company filings, Farside Investors, Spartan estimates.

The first indication came on July 6, when an 8-K disclosed that Strategy had sold 3,588 BTC ($216 million). Bitcoin dipped on the headline, then reversed within hours to above where it traded before the framework was announced. With roughly 26 months of dividend coverage, accretive buybacks available across the capital structure for the first time, and 843,775 BTC of collateral, fears of Strategy becoming a capitulatory forced seller are overblown. The more likely and boring answer is that they must gradually unwind their capital stack through a mixture of opportunistic BTC sales and MSTR / STRC re-purchases. While that process stabilizes the balance sheet, it also weakens the reflexive upside potential of MSTR, dampening the attraction which drew so many investors to it in the first place.

To learn more about investment opportunities with Spartan Capital, please contact ir@spartangroup.io